76

Navigating the Complexities of Bankruptcy Management for Servicers

12/14/2023 08:00 AM

Posted by: AIS

Servicers face significant challenges in managing bankruptcies, especially when dealing with mortgages, auto loans, and other consumer loans. These proceedings can be complex, requiring a nuanced understanding and strategic approach to mitigate risks and ensure efficient processing.

&nbps;

70

Key Criteria for Auto Lenders and Servicers When Evaluating Bankruptcy Servicing Partners

10/02/2023 08:00 AM

Posted by: AIS

Outsourcing certain back-office processes can give auto lenders a considerable edge. However, not all service providers are made equal. When looking externally for bankruptcy process management support, it's essential to find a servicing partner that understands the operational and compliance challenges associated with the bankruptcy system.

&nbps;

69

Unlocking Efficiency Through Business Process Outsourcing

09/28/2023 08:00 AM

Posted by: AIS

In today's dynamic business landscape characterized by shifting markets, rigorous regulatory standards, and economic challenges, maintaining a competitive edge is paramount. Business Process Outsourcing has emerged as an effective lever for companies to pull, ensuring streamlined operations and consistent growth.

&nbps;

68

Understanding Cost, Quality, and Scale: The Essentials for Outsourcing in the Mortgage Industry

09/26/2023 08:00 AM

Posted by: AIS

In our ever-evolving digital landscape, the challenge for many mortgage organizations lies in mastering cost efficiency, ensuring high-quality services, and scaling operations. Outsourcing has emerged as a powerful strategy to address these challenges.

&nbps;

67

From Loan Origination to Bankruptcy: Steering with Risk, Diligence, and Audits

09/19/2023 08:00 AM

Posted by: AIS

Whether you're a boutique mortgage servicer or an industry giant, risk management, due diligence, and audits are the cornerstones that ensure smooth operations and compliance. Let's delve into why these components are so crucial in the world of mortgage.

&nbps;

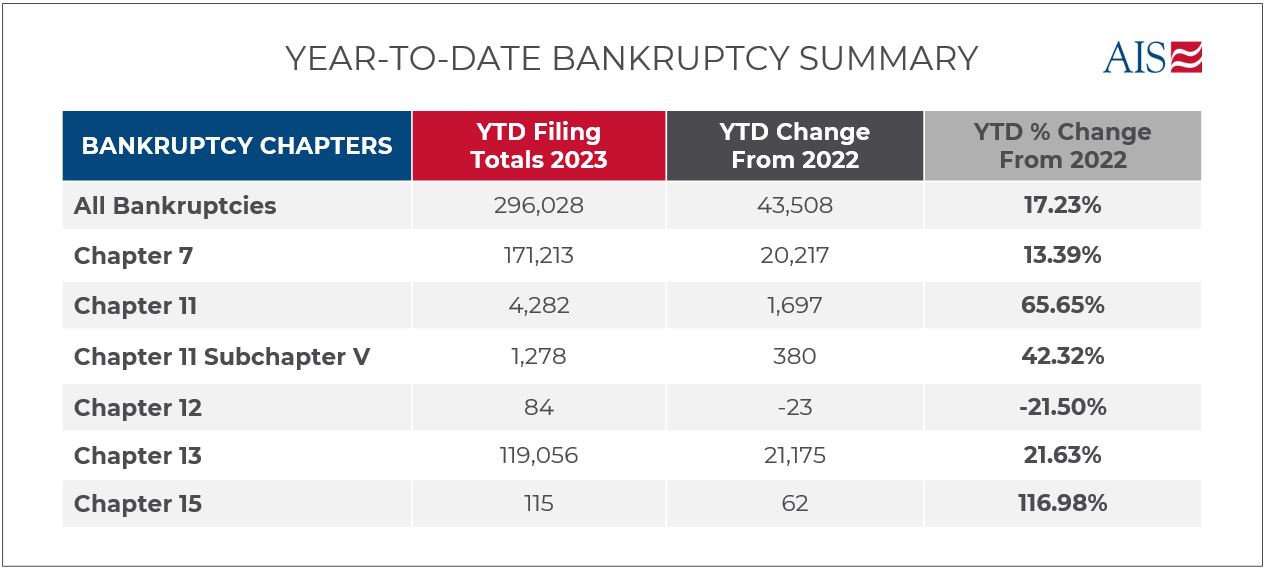

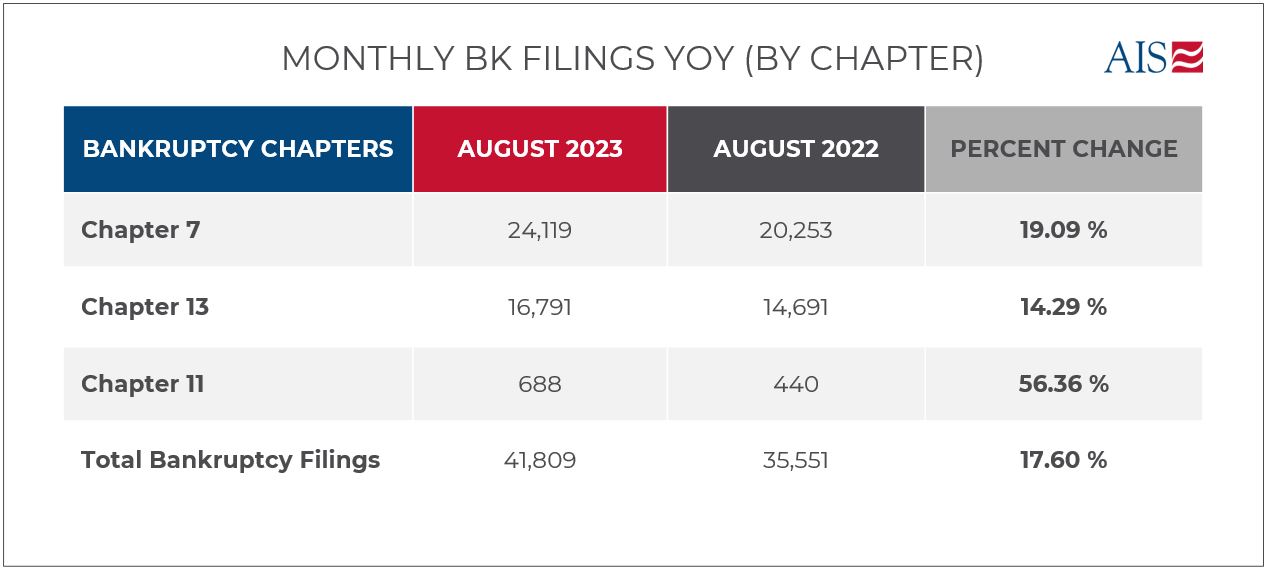

59

Are Bankruptcies Rising or Exploding?

09/12/2023 03:00 PM

Posted by: AIS

Bankruptcy filings in August totaled 41,809, marking a 17.60% increase from August 2022. Concurrently, there was a notable 56.4% spike in Chapter 11 filings, with small businesses under Subchapter V experiencing a 36.4% surge. Chapter 7 filings were up 19.09%, marking the second consecutive month 7s rose more than 13s. These escalating trends, particularly in Chapter 11, indicate looming broader economic concerns.

&nbps;

66

How Managed Services Pave the Way for Robotic Process Automation in the Mortgage Industry

09/12/2023 08:00 AM

Posted by: AIS

Two pivotal players are revolutionizing the mortgage industry: Managed Service Providers (MSPs) and Robotic Process Automation (RPA). AIS President, Tom Clark, explores the synergies between these two entities and how they're propelling the mortgage sector forward.

&nbps;

65

The Vital Role of Compliance and Quality in Mortgage Servicing

09/05/2023 08:00 AM

Posted by: AIS

In today's challenging landscape, the mortgage industry is grappling with stringent regulations that demand an unparalleled focus on compliance and quality. The regulatory environment has never been stricter, emphasizing the critical role of both digital and human capabilities.

&nbps;

61

Discovering a Better Way: AIS's Fast, Easy-to-Implement Banking Solutions

09/01/2023 08:00 AM

Posted by: AIS

For many banks, the idea of investing millions to explore large banking transformation initiatives might sound daunting and often unfeasible. As the market fills with vendors and consultants offering these complex solutions, it's essential to know that there's a different path available.

&nbps;

64

Ensuring Compliance and Quality with AIS: Your Go-To Partner for Mortgage Services

08/29/2023 08:00 AM

Posted by: AIS

Outsourcing critical business processes to Managed Services Providers (MSPs) is not just about delegation. It’s about partnership, trust, and ensuring utmost quality. Especially when it comes to sectors as regulated as the mortgage industry, the stakes are high. AIS stands out in its commitment to compliance and quality. But how does AIS compare, and what should you look out for in a quality compliance partner?

&nbps;

60

Important Updates on SBRA

08/22/2023 08:00 AM

Posted by: AIS

Over the past year, total bankruptcy filings have risen by 17%. Notably, small business filings under subchapter V, which accelerates the process, have surged by 44%. Congress will soon review SBRA eligibility, a crucial decision for both small businesses and creditors.

&nbps;

63

Unveiling the 90-Day Transformation Blueprint for Financial Service Providers

08/15/2023 08:00 AM

Posted by: AIS

In an era where staying ahead of the competition is paramount, CEOs and COOs in the financial sector constantly scout for methodologies that catalyze growth and streamline operations.Derived from a recent AIS executive brief that sheds light on strategic business transformations, this blog will walk you through a 12-week transformational journey tailored for financial service providers, aimed at reducing operational expenses and propelling revenue growth.

&nbps;

62

Optimizing Bankruptcy Management in Modern Banking

08/08/2023 08:00 AM

Posted by: AIS

Understanding and managing bankruptcy remains a pivotal task, especially for consumer banking and mortgage servicing sectors confronted with intricate regulatory frameworks. Drawing from the lessons of past financial downturns, the current digital and omnichannel environment offers a unique blend of challenges and growth prospects.

&nbps;

57

The Trend Holds: Bankruptcy Filings Are Up

07/05/2023 08:00 AM

Posted by: AIS

The June bankruptcy filing numbers are in, and they show a continued upward spiral. Total bankruptcies numbered 37,922, or 17.42 percent above the number posted last June. For the first half of 2023, bankruptcies rose by 17.36 percent over the first six months of last year. When will these steep increases end?

.JPG)

.JPG)

&nbps;

58

Important Updates on Federal Student Loans

07/04/2023 08:00 AM

Posted by: AIS

One of the potential accelerants that may further fuel the fire of increased bankruptcy filings is student loan debt. Currently, more than 40 million Americans owe about $1.7 trillion in outstanding student loans. The federal government's repayment pause due to the pandemic is ending soon, thanks to a recent debt ceiling compromise mandating repayment resumption from October. This could strain many household budgets.

&nbps;

56

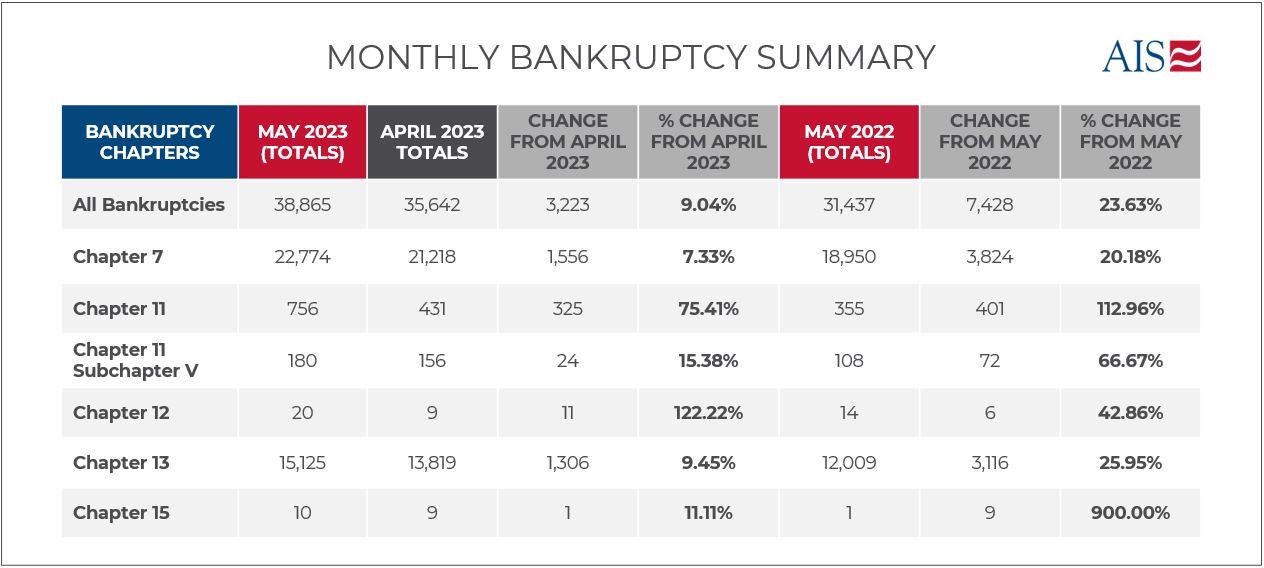

Bankruptcy Filings Way Up in May; Government Says They May Be Headed Much, Much Higher

06/05/2023 08:00 AM

Posted by: AIS

Bankruptcy filings went up by 23.6 percent in May compared to the same time period in 2022. The Department of Justice officially estimates that filings could double from pre-pandemic lows before the end of the calendar year 2025.

&nbps;

51

The Role of Managed Services in Driving the Adoption of RPA in Commercial Banking

05/22/2023 08:00 AM

Posted by: AIS

Tom Clark delves into the crucial role that Managed Service Providers (MSPs) play in fostering operational efficiency and scalability within banking. Highlighting the strategic use of MSPs in implementing Robotic Process Automation (RPA), he offers rich insights and guidance for financial institutions considering such initiatives.

&nbps;

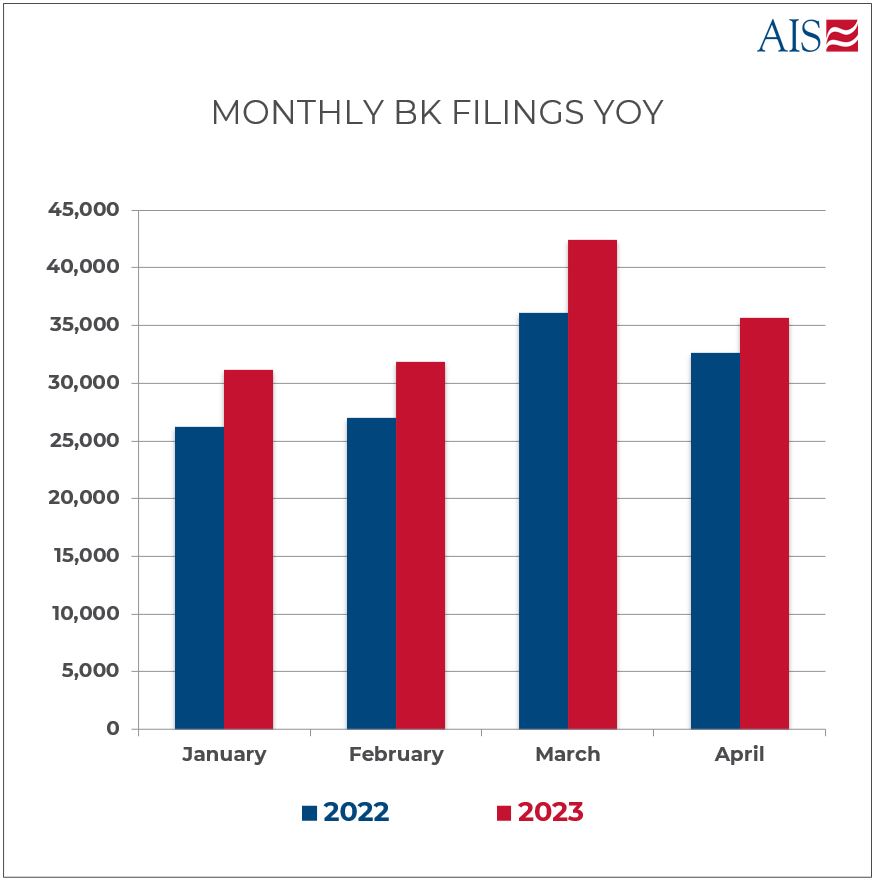

54

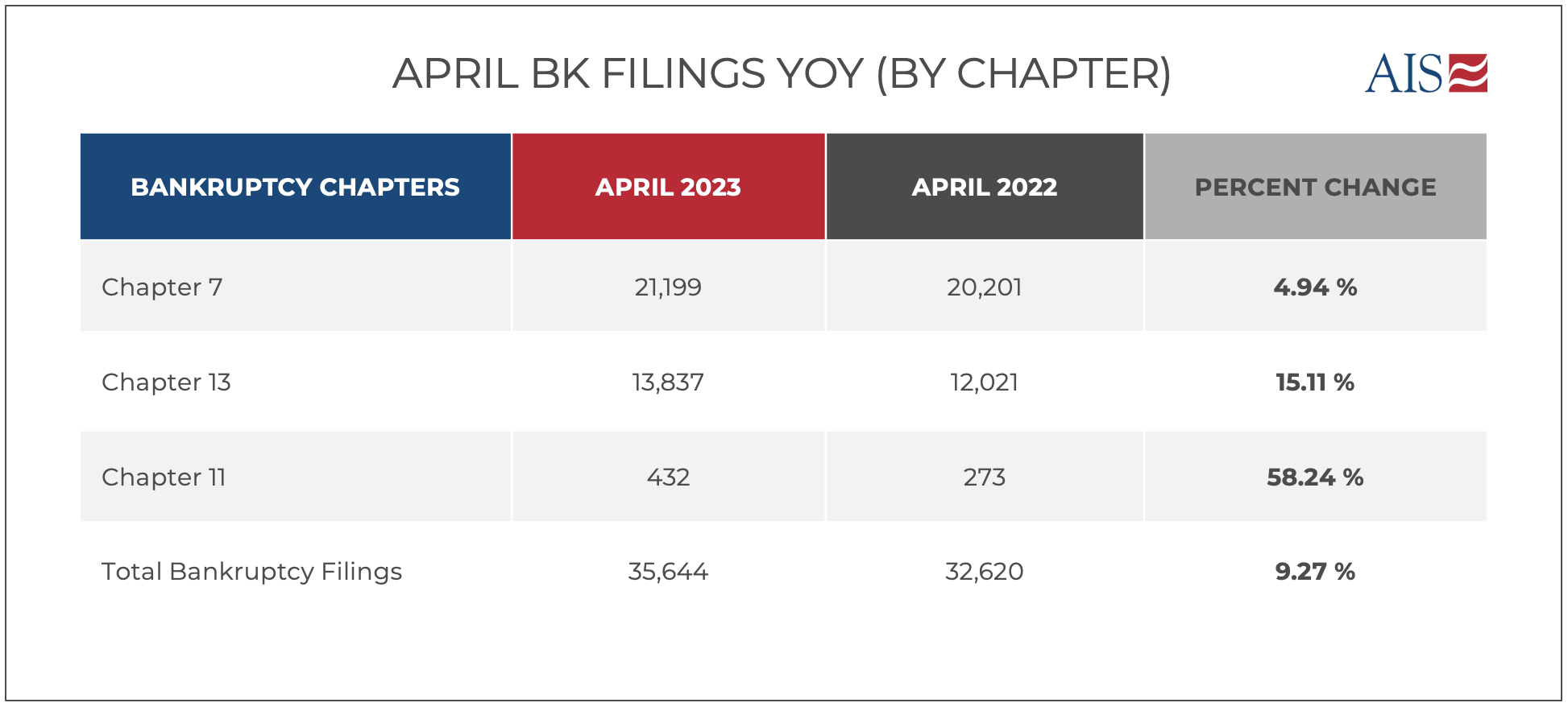

Bankruptcy Filings Continue Year Over Year Increases

04/04/2023 08:00 AM

Posted by: AIS

Total bankruptcy filings in April rose by 9.3 percent compared to the same month last year. This is the ninth consecutive month of overall filing increases. The rate of increase was less than last month’s increase, but March often reflects the response to the shock of holiday bills. Total filings for the first four months of 2023 are up by 15.7 percent over last year. This data analysis reinforces that the American bankruptcy system had better prepare for a sustained period of significant filing increases.

&nbps;

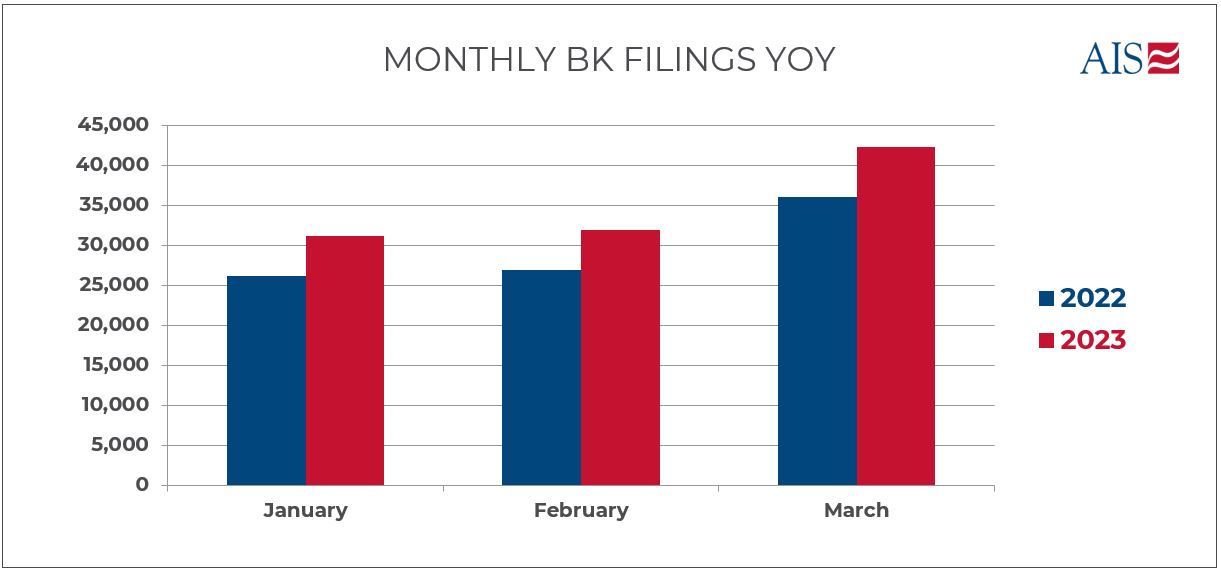

53

Bankruptcy Filings Flying Higher and Higher

04/04/2023 08:00 AM

Posted by: AIS

With the number of bankruptcy filings now in for the first calendar quarter of 2023, we know that the rapid rise in the number of individuals and companies seeking bankruptcy relief continues unabated. From January through March of this year, 18.1 percent more bankruptcy petitions were filed compared to the same period in 2022. In March alone, overall filings increased by 17.5 percent. This is the third consecutive month of year-over-year filing increases.

.JPG)

&nbps;

52

What About the Bankruptcy Fall-Out From Recent Bank Collapses?

03/22/2023 08:00 AM

Posted by: AIS

With the failure of Silicon Valley Bank (SVB) and Signature Bank, many in the bankruptcy community ask what – if any – impact there will be on bankruptcy filings and the bankruptcy system. Take a look at a snapshot of some of the issues and impacts being discussed.

&nbps;

Blog Search

Categories

Archives

202404April1

April 2024 (1)

202403March1

March 2024 (1)

202402February1

February 2024 (1)

202401January1

January 2024 (1)

202312December2

December 2023 (2)

202311November1

November 2023 (1)

202310October2

October 2023 (2)

202309September7

September 2023 (7)

202308August4

August 2023 (4)

202307July2

July 2023 (2)

202306June1

June 2023 (1)

202305May1

May 2023 (1)

202304April2

April 2023 (2)

202303March2

March 2023 (2)

202302February2

February 2023 (2)

202301January1

January 2023 (1)

202212December2

December 2022 (2)

202211November1

November 2022 (1)

202210October2

October 2022 (2)

202209September2

September 2022 (2)

202208August1

August 2022 (1)

202207July2

July 2022 (2)

202206June2

June 2022 (2)

202205May1

May 2022 (1)

202203March2

March 2022 (2)

202202February1

February 2022 (1)

202201January1

January 2022 (1)

202112December1

December 2021 (1)

202111November1

November 2021 (1)

202110October1

October 2021 (1)

202107July1

July 2021 (1)

202106June1

June 2021 (1)

202105May1

May 2021 (1)

202104April1

April 2021 (1)

202101January1

January 2021 (1)

202012December2

December 2020 (2)

202011November1

November 2020 (1)

202010October1

October 2020 (1)

202009September1

September 2020 (1)

202008August1

August 2020 (1)

202007July1

July 2020 (1)

202006June3

June 2020 (3)

202005May3

May 2020 (3)

202004April2

April 2020 (2)