| ||

54https://www.aisinfo.com/blog/2023/04/ais-insight-blog-april-2023

Bankruptcy Filings Continue Year Over Year Increases

04/04/2023 08:00 AM

Posted by: AIS

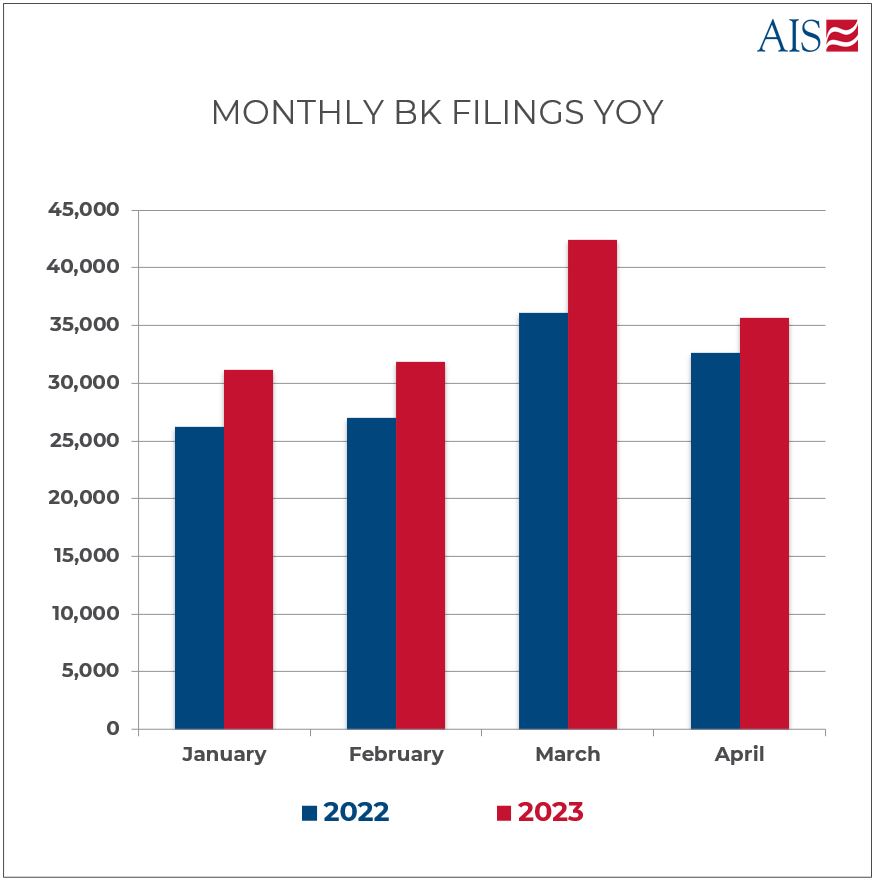

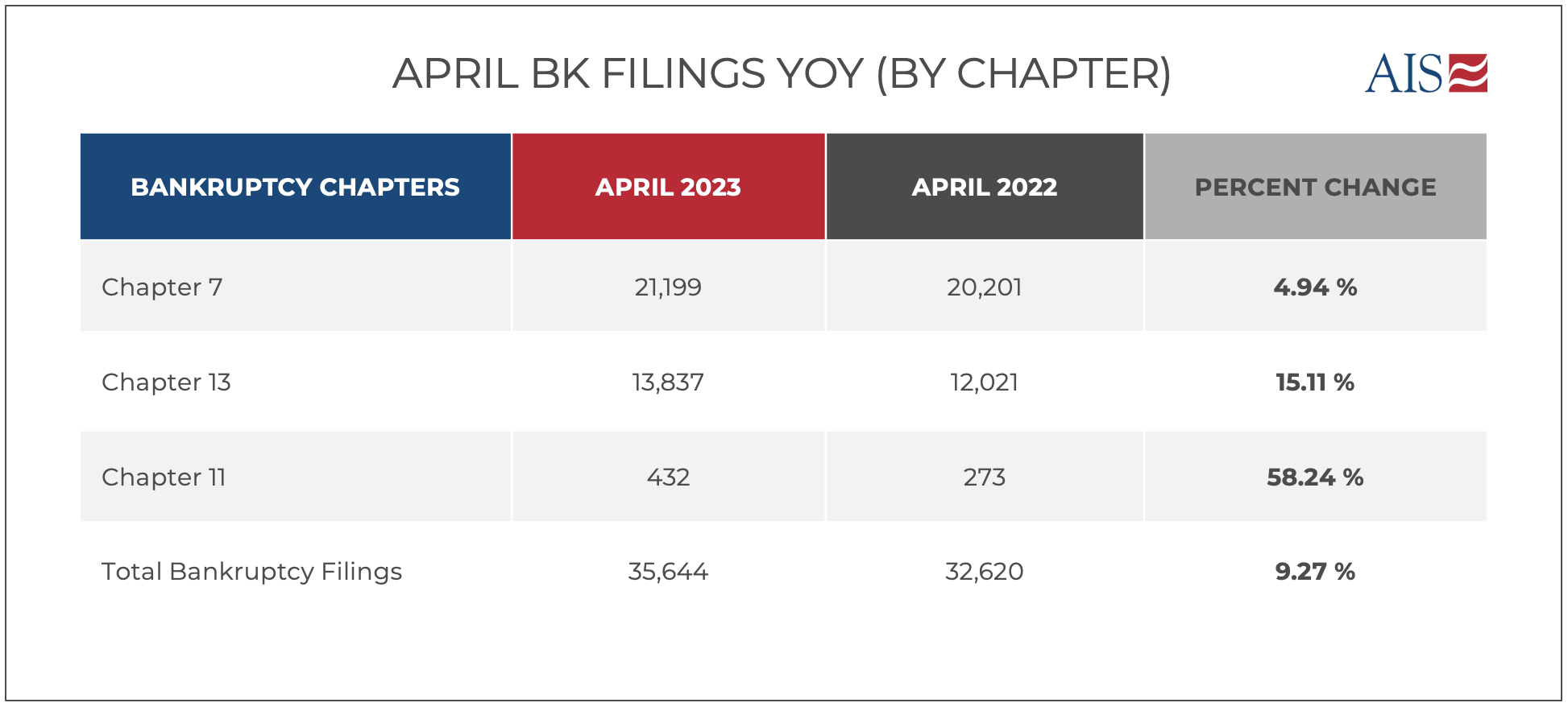

Total bankruptcy filings in April rose by 9.3 percent compared to the same month last year. This is the ninth consecutive month of overall filing increases. The rate of increase was less than last month’s increase, but March often reflects the response to the shock of holiday bills. Total filings for the first four months of 2023 are up by 15.7 percent over last year. This data analysis reinforces that the American bankruptcy system had better prepare for a sustained period of significant filing increases.

Breakdown of Data by Major Chapter Chapter 13 cases filed in April rose by another 15.1 percent compared to last year, which is remarkable given the extraordinary growth we already have seen. Moreover, the most recent talk in trustee and consumer attorney circles is that previous home value increases have provided debtors with substantial home equity, even in spite of the recent cooling of home sales. Add to that mortgage interest rates that are unaffordable and less available, and chapter 13 makes even more economic sense for homeowners. Chapter 11s went up by a very strong 58.2 percent over last April, albeit led by the multiple filings made by Bed, Bath & Beyond. The stress on corporations is increasingly apparent. This is even more so with Subchapter V small business filings, which rose by a stratospheric 85.9 percent compared to last year. The strain of high interest rates and restrictive lending may be showing most conspicuously in the small business numbers.

Round-Up of Some Significant Economic Data Points Beyond the now obvious reasons for the rise in consumer filings (namely, the government exploded all past records of government cash and other assistance during COVID), other economic reports in April continue to flash warning signs about what is on the horizon. These signs are ominous regardless of whether the national economy falls into an officially declared recession. Here are a few signs worth noting:

Macroeconomic and corporate bond trends do not always follow a straight line with bankruptcy filings, but a drill down on consumer credit news also yields major red flags. Although the quality of credit portfolios varies markedly among lenders, evidence of previously reported expansions of consumer credit continues to lead to more negative reports on consumer debtor defaults. A Businessweek headline sums up some of the recent news: "The Repo Man Returns as More Americans Fall Behind on Car Payments.” Fitch ratings show more than a doubling of subprime auto borrowers who were 60 days or more delinquent in making payments compared to the May 2021 pandemic low. That is higher than the delinquency rate at the height of the Great Recession. (Source: Clare Ballentine, Businessweek, 4/19/23.) Added to all this are anecdotal reports that bankruptcy practices are receiving more regulatory scrutiny. That is exactly what happened when filings rose during the Great Recession. One difference is that there is another cop on the block this time. The CFPB now has supervisory powers over banking institutions that it has no hesitation in using. CFPB views its scope as encompassing violations of both bankruptcy and consumer protection laws. Another cautionary note: debtor counsel can also expect to be more aggressive. A recent unpublished decision illustrates the point. In Orlansky v. Quicken Loans, BAP No. NV-22-1181 (filed April 14, 2023), a debtor challenged the monthly mortgage statement sent to debtors for incorrectly placing its notice of pre-petition fees. The Bankruptcy Appellate Panel reversed a bankruptcy court decision and found a violation of the automatic stay. In that case, the court expects damages to be "relatively minimal.” (Kudos to Bill Rochelle of the American Bankruptcy Institute for flagging the case in his daily report posting on the ABI website.) Conclusion Here’s a wrap-up for April: Bankruptcy filings are climbing higher than most analysts expected. General economic news is ominous, including for consumer lending. As expected, regulators are perched and ready to pounce. So, auto and mortgage lenders beware.

Commentary provided by Clifford J. White, Managing Director – Bankruptcy Compliance for AIS.

Blog Search

CategoriesArchives

202404April1

April 2024 (1)

202403March1

March 2024 (1)

202402February1

February 2024 (1)

202401January1

January 2024 (1)

202312December2

December 2023 (2)

202311November1

November 2023 (1)

202310October2

October 2023 (2)

202309September7

September 2023 (7)

202308August4

August 2023 (4)

202307July2

July 2023 (2)

202306June1

June 2023 (1)

202305May1

May 2023 (1)

202304April2

April 2023 (2)

202303March2

March 2023 (2)

202302February2

February 2023 (2)

202301January1

January 2023 (1)

202212December2

December 2022 (2)

202211November1

November 2022 (1)

202210October2

October 2022 (2)

202209September2

September 2022 (2)

202208August1

August 2022 (1)

202207July2

July 2022 (2)

202206June2

June 2022 (2)

202205May1

May 2022 (1)

202203March2

March 2022 (2)

202202February1

February 2022 (1)

202201January1

January 2022 (1)

202112December1

December 2021 (1)

202111November1

November 2021 (1)

202110October1

October 2021 (1)

202107July1

July 2021 (1)

202106June1

June 2021 (1)

202105May1

May 2021 (1)

202104April1

April 2021 (1)

202101January1

January 2021 (1)

202012December2

December 2020 (2)

202011November1

November 2020 (1)

202010October1

October 2020 (1)

202009September1

September 2020 (1)

202008August1

August 2020 (1)

202007July1

July 2020 (1)

202006June3

June 2020 (3)

202005May3

May 2020 (3)

202004April2

April 2020 (2) | ||