| ||

34https://www.aisinfo.com/blog/2022/07/ais-insight-blog-june-2022

Chapter 13, 11 Filings Continue to Rise in June

07/12/2022 03:13 PM

Posted by: AIS

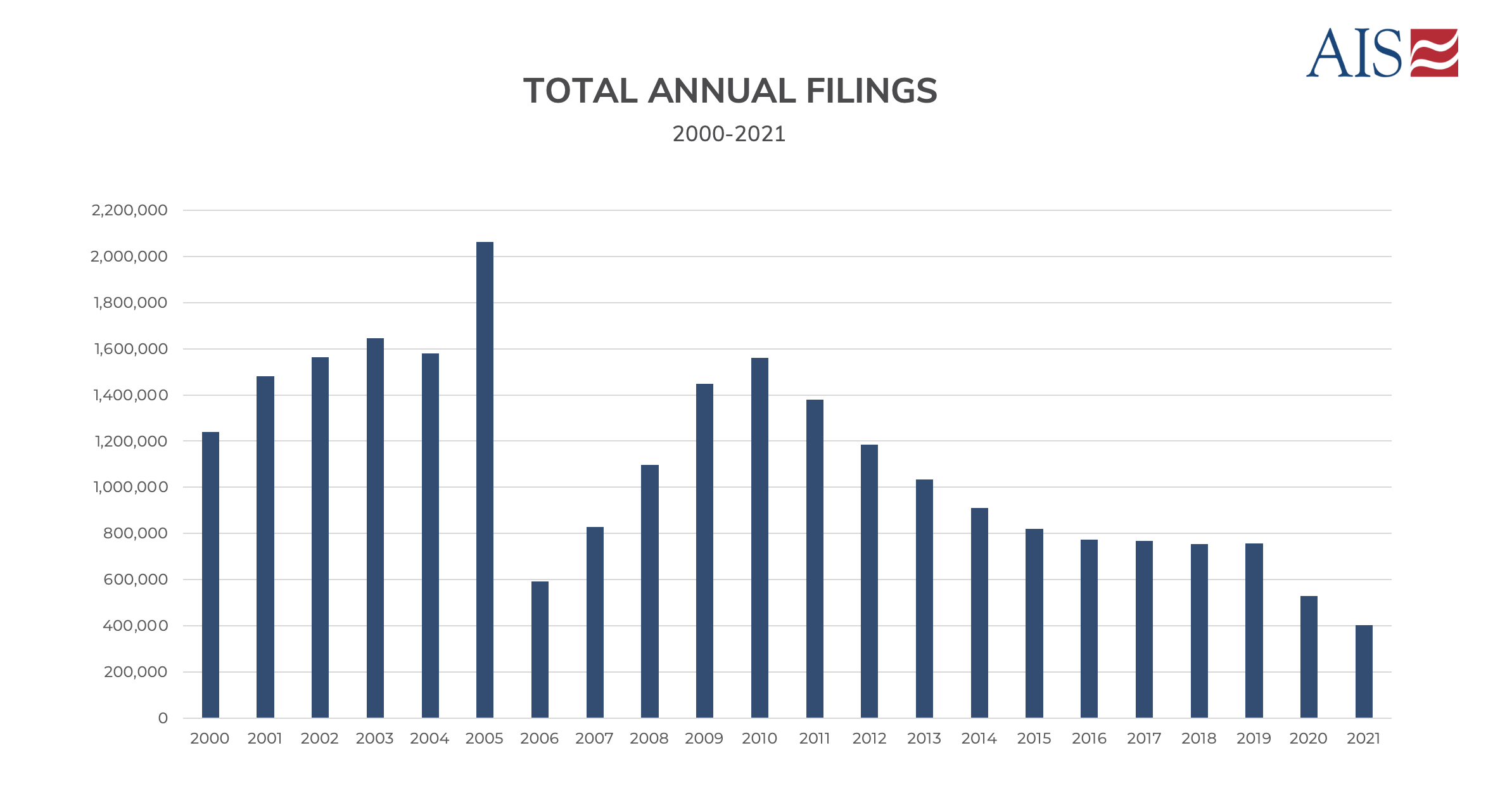

Is the Era of Low Bankruptcy Filings About to End? This is the time to Prepare.Bankruptcy filings have been at historic lows since the beginning of the COVID pandemic in 2020. But deteriorating national economic conditions and recent chapter 13 filing data suggest that bankruptcy increases may be on the horizon. If history is any guide, then more scrutiny of creditors’ compliance with bankruptcy and consumer protection laws and rules can be expected as well. All this may make it a good time for financial institutions and other creditors to review their bankruptcy processes to reduce the risk they will come under the regulatory microscope. Historical Bankruptcy Filing Rates Although predicting bankruptcy filing rates may be more hazardous than at any time in recent memory, it is worth noting that filings have been gyrating over many years. For example, 40 years ago bankruptcy filings stood at 380,000 cases. Last year, they reached about 414,000, or 18 percent above the low-water mark of the past five decades. But charting filing numbers between those years is a lot like drawing a rollercoaster. The graph below (Figure 1) shows bankruptcy filing numbers for the past 20 years. In the 1990s, bankruptcy filings climbed above million. As the chart shows, they continued to climb until they exceeded two million cases in 2005. That number was somewhat artificial, however, because Congress sought to reduce the precipitous increase in filings by passing the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005, which imposed a means test and made other significant changes in the law. Many lawyers tried to beat the effective date of the 2005 amendments by urging their clients to file sooner. Debtors did exactly that. Of course, that led to a sharp drop in filings the next year. Filings then began to rise to more normalized levels. The next blip on the chart occurs in about 2008-2010 during the Great Recession when external economic conditions drove filings skyward. After that, filings leveled off and changed very little from about 2016-2019. Then the COVID pandemic hit. Many of us predicted that the pandemic would cause a large increase in filings. I was wrong. Instead, as Figure 1 shows, the numbers dropped – by a lot. In retrospect that is not surprising because the amount of government cash and other assistance, including foreclosure and eviction moratoria, were unprecedented. But there are new signs that filing patterns are changing.

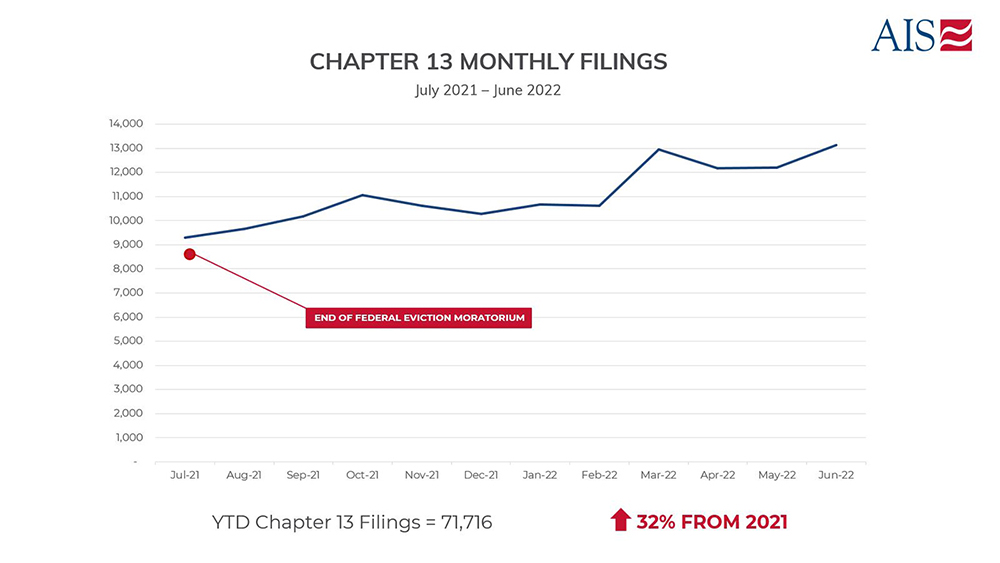

Figure 1 Chapter 13 Filing Increases Figure 2 charts the past 12 months of chapter 13 filings. Insofar as chapter 13 is designed for individuals with a regular income, many of whom have fallen behind on secured debt payments and still want to save their home or car, one might expect home foreclosure and eviction moratoria to influence filing rates strongly. Figure 1 suggests exactly that. The federal eviction moratoria generally ended last July. That is where our chart begins. As the trend line shows, chapter 13 file rates are up significantly over the past 12 months. Comparing January to June rates alone, the 2022 filing rates are 32 percent above the previous year. In light of other economic conditions, this increase may forebode future increases as well, at least in chapter 13.  Figure 2 Deteriorating Economic Conditions In addition to the expiration of government aid, which eventually will have an impact on many economically vulnerable consumers who were able to delay the day of financial reckoning, macroeconomic conditions are unfavorable. For the first time since the late 1970s through 1982, we are seeing high inflation, rising interest rates, and perhaps slowing economic growth. In early June of this year, the World Bank (along with many economic mavens) warned of "stagflation.” And Chase CEO Jamie Dimon said there is an economic "hurricane” heading our way. Since those prognostications were uttered, national economic data have not painted a brighter picture. Reduce Regulatory Risk The last time we faced a sharp economic downturn, federal regulators enhanced their scrutiny of bankruptcy and other creditor practices. Among things, this culminated in a $25 billion national mortgage settlement and many other multi-million-dollar bankruptcy settlements pertaining to the accuracy of proofs of claim for secured and unsecured debt alike. Perhaps more expensive in the long-run than remediation to consumer debtors, regulatory relief sometimes entailed injunctive relief (e.g., monitors to review internal creditor practices) and severe reputational damage.With filings still relatively low, and regulatory actions concomitantly lower, this may be a good time for creditors to perform a check-up on their bankruptcy compliance systems to make sure they can withstand future regulatory scrutiny. Conclusion All reputable creditors want to treat consumer fairly and in compliance with law. But even the best of systems for handling distressed accounts need a check-up every now and again to be sure faulty practices did not seep in. Now may be a good time for a regulatory refresh before Jamie Dimons’s predicted "hurricane” hits consumers and creditors alike. To download the June Insight Report, click here. Blog Search

CategoriesArchives

202404April1

April 2024 (1)

202403March1

March 2024 (1)

202402February1

February 2024 (1)

202401January1

January 2024 (1)

202312December2

December 2023 (2)

202311November1

November 2023 (1)

202310October2

October 2023 (2)

202309September7

September 2023 (7)

202308August4

August 2023 (4)

202307July2

July 2023 (2)

202306June1

June 2023 (1)

202305May1

May 2023 (1)

202304April2

April 2023 (2)

202303March2

March 2023 (2)

202302February2

February 2023 (2)

202301January1

January 2023 (1)

202212December2

December 2022 (2)

202211November1

November 2022 (1)

202210October2

October 2022 (2)

202209September2

September 2022 (2)

202208August1

August 2022 (1)

202207July2

July 2022 (2)

202206June2

June 2022 (2)

202205May1

May 2022 (1)

202203March2

March 2022 (2)

202202February1

February 2022 (1)

202201January1

January 2022 (1)

202112December1

December 2021 (1)

202111November1

November 2021 (1)

202110October1

October 2021 (1)

202107July1

July 2021 (1)

202106June1

June 2021 (1)

202105May1

May 2021 (1)

202104April1

April 2021 (1)

202101January1

January 2021 (1)

202012December2

December 2020 (2)

202011November1

November 2020 (1)

202010October1

October 2020 (1)

202009September1

September 2020 (1)

202008August1

August 2020 (1)

202007July1

July 2020 (1)

202006June3

June 2020 (3)

202005May3

May 2020 (3)

202004April2

April 2020 (2) | ||